- Bloomberg – A $3 Trillion Credit Market Has Corporate Bond Investors on Edge

Notes rated BBB look increasingly vulnerable to some analysts

A huge swath of the corporate bond market is looking increasingly vulnerable. Bonds with the lowest investment grade have been a market darling over the past decade, ballooning in size as low global interest rates drew fund managers seeking higher returns. But as borrowing costs climb to a four-year high just as investors begin to anticipate a downturn in the global economy, some analysts are starting to sound the alarm. “We’re late in the credit cycle, and trying to figure out when everything turns,” said Erin Lyons, a senior credit strategist at New York-based research firm CreditSights Inc. “Some of these may eventually be downgraded.”

Summary

Comment

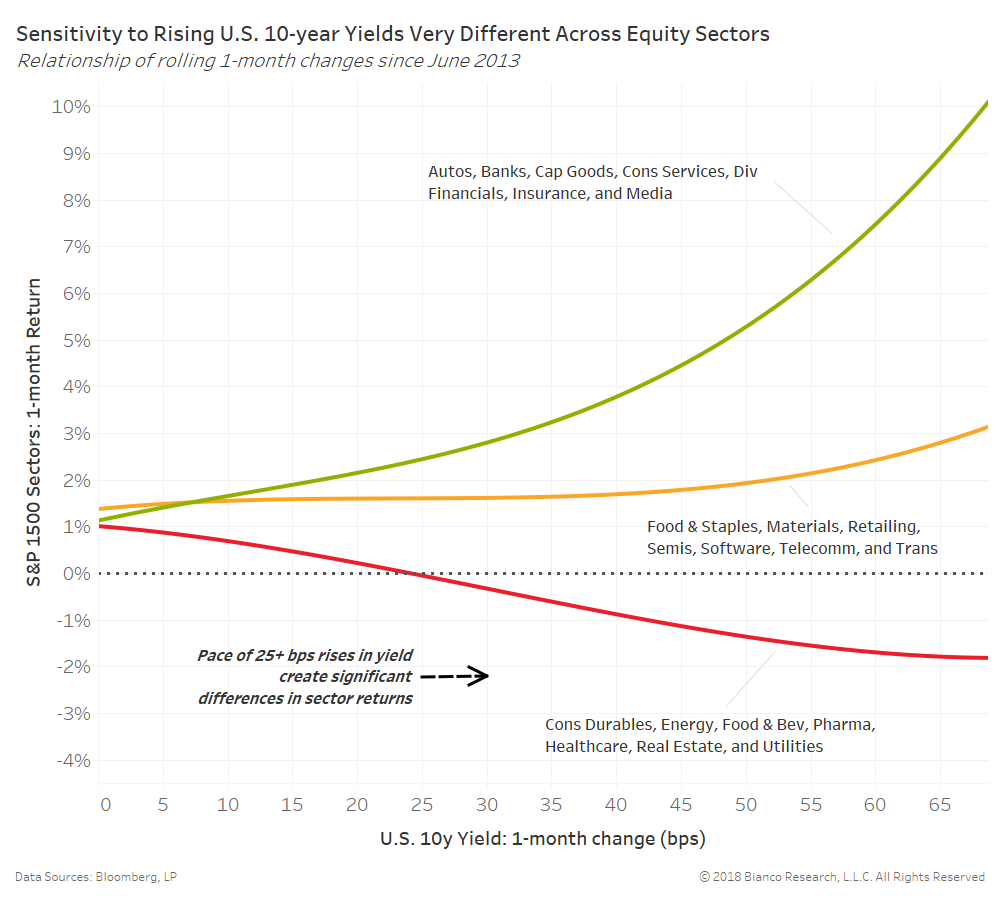

U.S. 10-year yields above 3.0% are resurfacing risks plaguing a potentially bloated credit market. The chart below shows rolling one-month changes in U.S. 10-year yields versus returns produced by S&P 1500 sectors since June 2013. We have grouped sectors with similar sensitivities to U.S. 10-year yields.

The pace of rising yields in excess of 25 bps has produced the greatest divergence in sector returns (see arrow on chart). Sectors underperforming in this scenario include consumer durables, energy, food & beverage, pharma, healthcare, real estate, and utilities. The current pace of rising yields is near 20 bps.

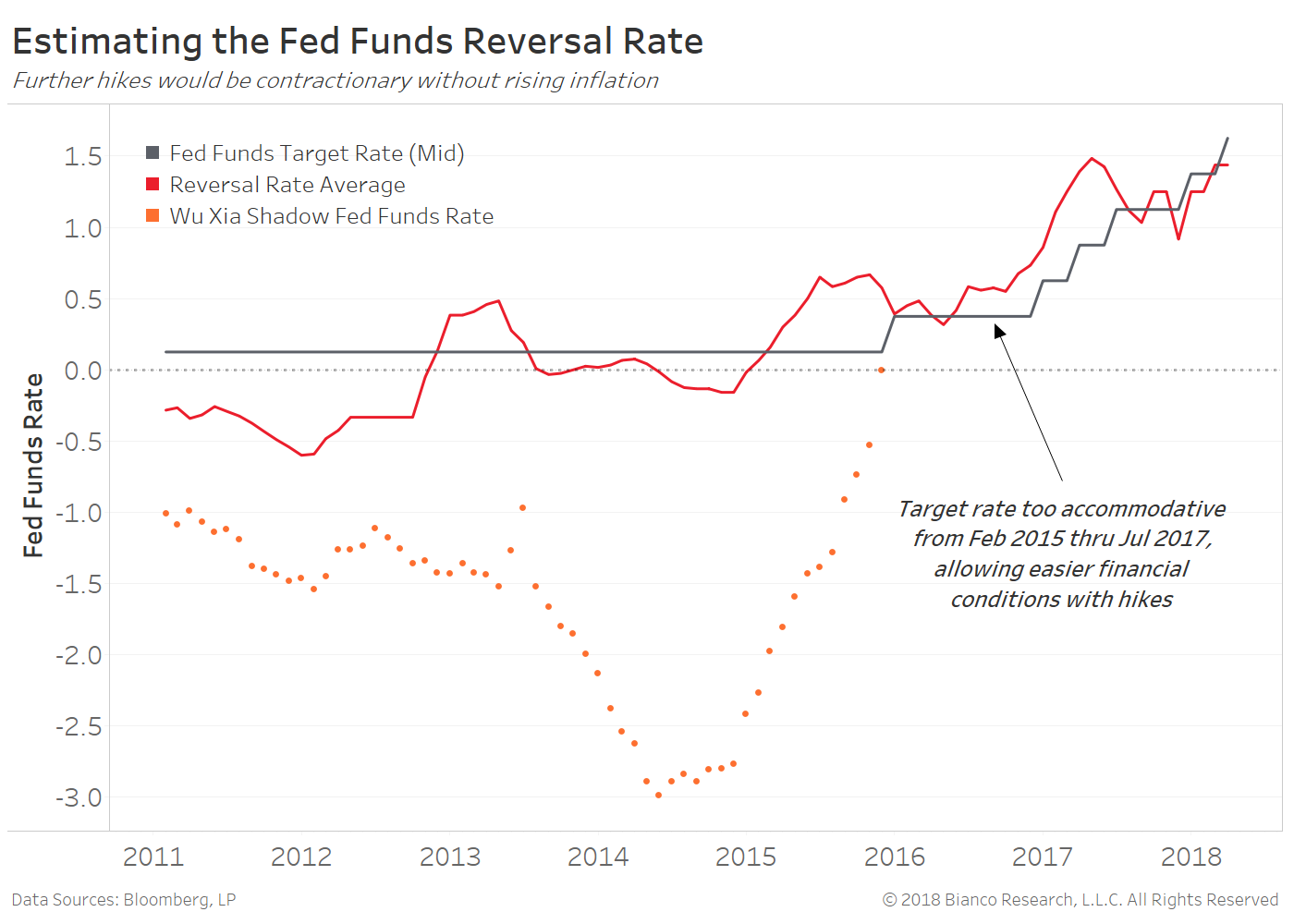

The critical concern above and beyond this 3.0% threshold is the fed funds rate relative to the neutral rate.

We estimate the reversal rate (or neutral rate) by stress testing lending growth and financial leverage with changes in the fed funds target rate. The rate leading to greater than 50% probability of causing a contraction in lending growth and financial leverage is marked the reversal rate, which currently resides near 140 bps (see chart below).

Economists are estimating core PCE, which is reported April 30th, will finally reach the elusive 2.0% year-over-year target. The removal of base effects due to cell phone and physicians’ services components have the potential to foster this 40 bps bump in core inflation through March 2018. Our estimates for the reversal rate would rise by nearly the same amount to roughly 180 bps, meaning the Fed has room for an additional hike in June 2018.

Unfortunately, the three-to-four hikes expected by the Fed over the next 12 months will be difficult to conduct without greatly impairing financial conditions. Languishing wage growth is still maintaining downward pressure on the neutral rate, which likely resides much lower than Powell et al believe.

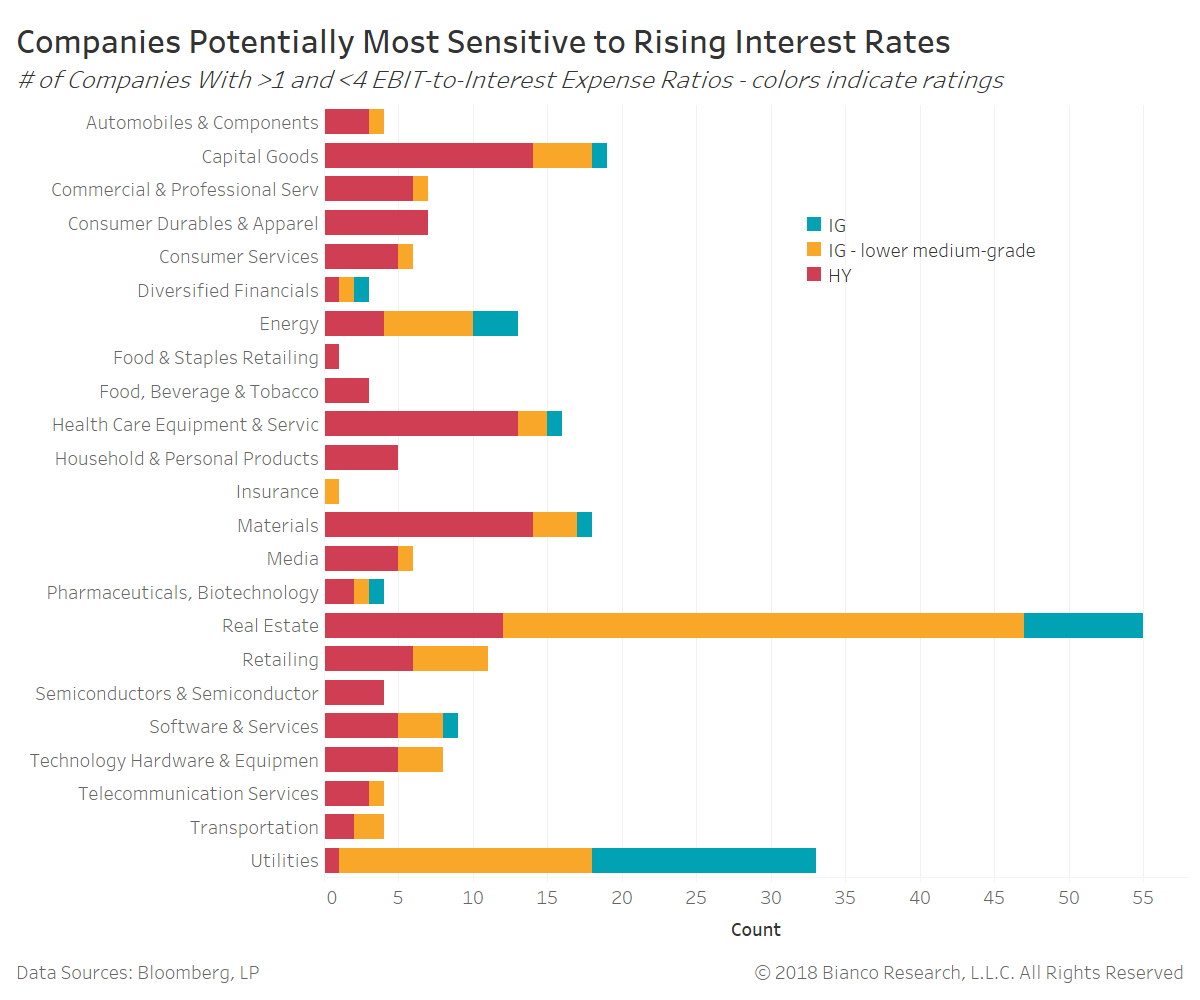

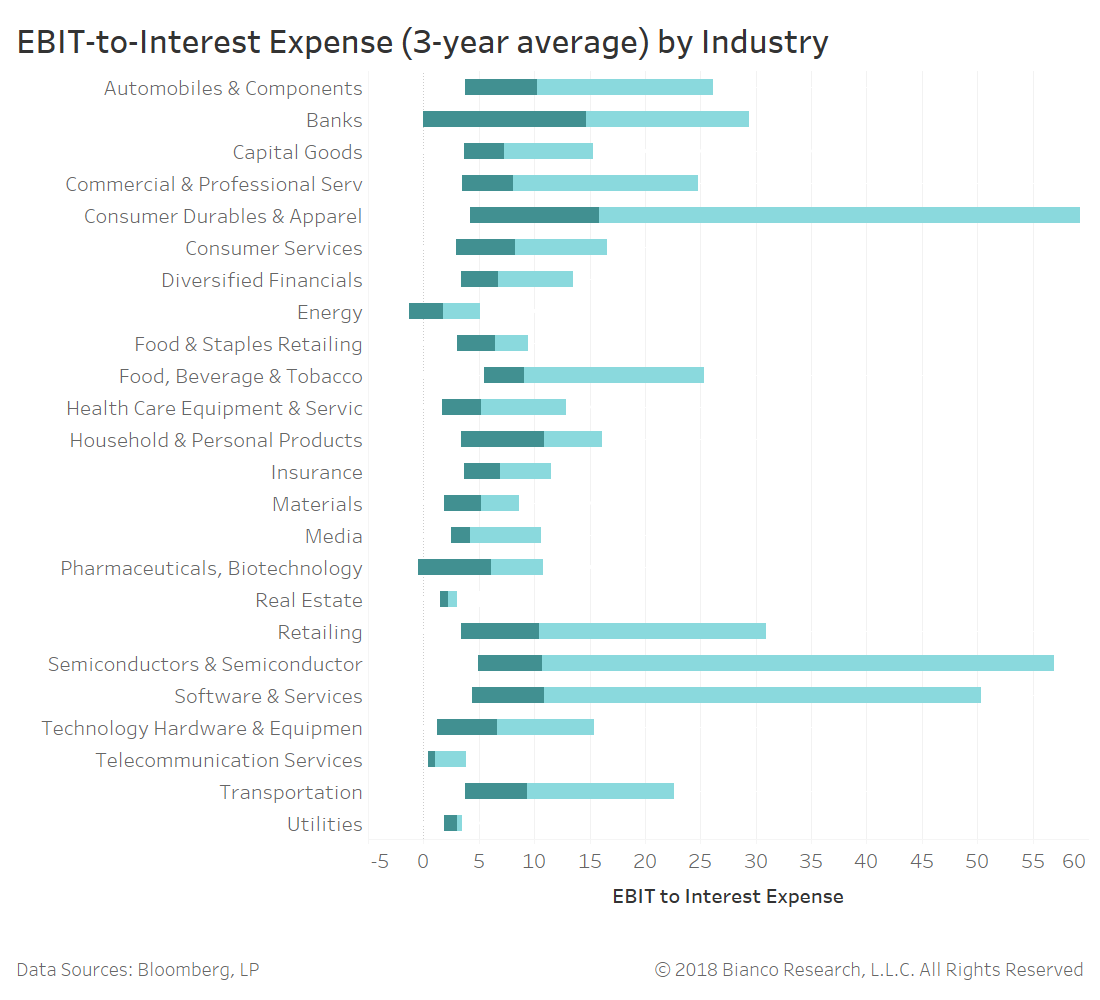

The double whammy of Fed tightening to and/or above the neutral rate and rising long-end yields would likely inflict pain on so-called zombie companies, which are companies with three-year average EBIT-to-interest expense ratios below one. A whopping 14% of the S&P 1500 can be dubbed ‘walking dead.’

The chart below shows the range (25th-75th percentiles) of EBIT-to-interest expense ratios for each industry group of the S&P 1500. Energy, real estate, telecom, and utilities have median ratios below five, well below other industries.

The next chart shows the number of companies within each industry susceptible to turning into zombies. These companies currently have EBIT-to-interest expense ratios between one and four. The colors represent a composite of major credit ratings:

- Blue = Prime through upper medium investment grade

- Orange = Lower rated investment grade

- Red = Non-investment grade

Capital goods, energy, materials, real estate, and utilities have higher numbers of companies with investment-grade ratings susceptible to becoming zombies. In other words, these are the sectors at greatest risk of numerous credit downgrades.