- CNBC – More of Wall St. sees a later rate hike: Survey

These are the times that try the souls of those forecasting a September rate hike. The latest monthly CNBC Fed Survey still shows a majority on Wall Street forecasting that first rate hike in nine years to come in September, but it’s a dwindling majority rife with defections to the later months of October and December. “The market seems to be saying ‘no’ even as the Fed is saying ‘yes’ to a near-term rate hike,” Kevin Giddis of Raymond James/Morgan Keegan wrote in response to the survey. “While the Fed ultimately has the stick, they really need the market to come along so we don’t find ourselves in a highly volatile limited liquidity aftershock of the Fed’s action.” Just over half of the survey’s 35 respondents of economists, fund managers and analysts, say the rate hike will come in September, down from 63 percent in the prior survey. And the forecast for the year-end Fed funds rate continues to decline, with the average now just 0.47 percent. Last July, Wall Street looked for a year-end funds rate just above 1 percent, showing how much tightening has been baked out of the market this year. To be sure, 82 percent say the Fed will hike this year, but that’s down from 92 percent in the prior survey.

Comment

<Click on graphic for larger image>

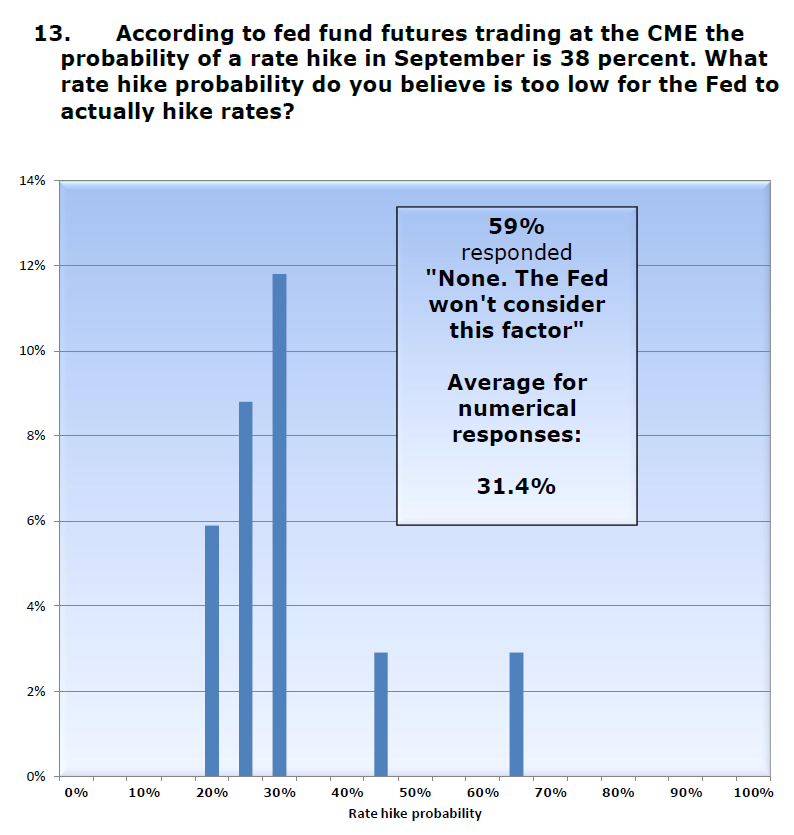

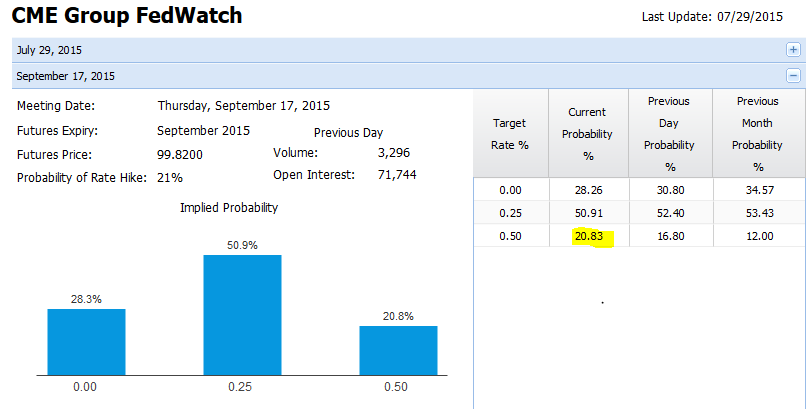

59% of respondents do not believe the Fed will consider market expectations when hiking. As regular readers know, we believe market expectations are hugely important to the Fed’s thinking. As the graphic below shows, the CME’s Fed Monitor puts the probability of a September hike at 20.83% (yellow highlight).

<Click on graphic for larger image>

Why do market expectations matter? We detailed this last month:

New York Federal Reserve President Bill Dudley said this [last month]:

Moreover, the appropriate stance of monetary policy will be influenced by how financial market conditions respond to the Federal Reserve’s actions. All else equal, if financial conditions tighten sharply, then we are likely to proceed more slowly. In contrast, if financial conditions were not to tighten at all or only very little, then—assuming the economic outlook hadn’t changed significantly—we would likely have to move more quickly. In the end, we will adjust the policy stance to support the financial market conditions that we deem are most consistent with our employment and inflation objectives.

We translate this to mean the Fed will be watching equity prices closely. Falling equity prices could prompt the Fed to get more accommodative while stable-to-rising equity prices give the Fed an all-clear signal to continue raising rates. Note that he did not say anything about the economy.

This kind of comment is not new for Dudley. Last December he said:

“With respect to “how fast” the normalization process will proceed, that depends on two factors—how the economy evolves, and how financial market conditions respond to movements in the federal funds rate target. Financial market conditions mainly include, but are not necessarily limited to, the level of short- and long-term interest rates, credit spreads and availability, equity prices and the foreign exchange value of the dollar. When the FOMC adjusts its short-term federal funds rate target, this does not directly influence the economy since little economic activity is linked to the federal funds rate. Instead, monetary policy affects the economy as the current change in short-term interest rates and expectations about future monetary policy changes influence financial market conditions more broadly.

The question is how much “instability” in financial markets will/can the Fed tolerate? And why are they talking about equity prices and not interest rates? Consider what Bernanke said last [month] in his blog:

Stock prices have risen rapidly over the past six years or so, but they were also severely depressed during and just after the financial crisis. Arguably, the Fed’s actions have not led to permanent increases in stock prices, but instead have returned them to trend.

So, according to Bernanke, monetary policy has boosted stock prices and the Fed should proudly take credit for it. Further Bernanke said the Fed has boosted stock prices to a “good level” but has not overdone it to a “bad level” (we discussed this last week).

So will the Fed be willing to let equity prices fall after it worked so hard to boost them? In April Bernanke responded to a harsh criticism of monetary policy by concluding with:

We shouldn’t be giving up on monetary policy, which for the past few years has been pretty much the only game in town as far as economic policy goes. Instead, we should be looking for a better balance between monetary and other growth-promoting policies, including fiscal policy.

He also offered the following in a Jackson Hole speech in 2012:

Model simulations conducted at the Federal Reserve generally find that the securities purchase programs have provided significant help for the economy. For example, a study using the Board’s FRB/US model of the economy found that, as of 2012, the first two rounds of LSAPs may have raised the level of output by almost 3 percent and increased private payroll employment by more than 2 million jobs, relative to what otherwise would have occurred.

As well as this in a November 2010 Washington Post editorial:

Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.

The Fed thinks QE saved the world by creating millions of jobs and adding percentage points to GDP. It ramped stock prices higher, creating a wealth effect.

While we disagree with this diagnosis, it is important to understand the Fed thinks this way. This being the case, we can’t imagine they would upset the single metric that saved the economy. Restated, they will not do anything that will hurt stocks.

If this is the case, how does the Fed ever tighten? As we have said in the past, the markets must first price it in. That means the effects of higher rates are already baked into the market and the act does not become an event for markets but rather a formality. Given Dudley’s obsession with financial stability and Bernanke’s belief that QE has pushed stock prices to a “good level” that has created millions of jobs, the Fed is not going to fight the market and risk it all.

- Bloomberg.com – (October 2, 2012) Bernanke Seeks Gains for Stocks in Push for Jobs: Economy

Chairman Ben S. Bernanke is increasingly aiming for gains in stock prices as the Federal Reserve reaches for new tools to spur the three – year r ecovery and reduce unemployment stuck above 8 percent. Bernanke, setting the stage for a third round of quantitative easing in an Aug. 31 speech in Jackson Hole, Wyoming, said the strategy works in part by boosting the prices of assets such as equitie s. In a speech yesterday in Indianapolis he said higher stock and home prices would provide further impetus to spending by businesses and households. “ It’s pretty clear that the stock market is the most important transmission mechanism of monetary poli cy right now ,” said Peter Hooper, chief economist at Deutsche Bank AG in New York. “That’s where you’re getting most of the action in terms of lift to the economy. It’s the stock market that’s going to have to be carrying the load.” …

The week before every FOMC meeting, CNBC surveys about 50 economists and money managers about the Fed. The full survey is above.

We found the question below very interesting.