- CNBC – Fed Chair Powell says balance sheet decision market is waiting for is ‘close’ to happening

* Fed Chairman Jerome Powell said Wednesday the central bank is close to a timetable on when its balance sheet reduction will end.

* The balance sheet is currently just over $4 trillion, most of which is Treasurys and mortgage-backed securities bought to stimulate the economy.

* An announcement will be coming “fairly soon,” the central bank chief told House members.

* “We are not looking at a higher inflation target, full stop,” Powell also said - The Wall Street Journal – Powell Says Fed Is Close to Agreement on Plan to End Portfolio Runoff

Federal Reserve Chairman Jerome Powell said Wednesday the central bank is close to announcing plans for ending the runoff of its $4 trillion portfolio of bonds and other assets this year. “We’re going to be in a position…to stop runoff later this year,” Mr. Powell told members of the House Financial Services Committee. Mr. Powell said Fed officials are near agreement on a plan. “My guess is we’ll be announcing something fairly soon,” he said. The Fed’s rate-setting committee next meets on March 19-20.

Summary

Comment

We have argued the Fed and the markets have not been on the same page regarding the effect balance sheet reductions have on the markets. Jay Powell has tried to downplay their importance many times, going as far as saying the QT process is, “like watching paint dry.”

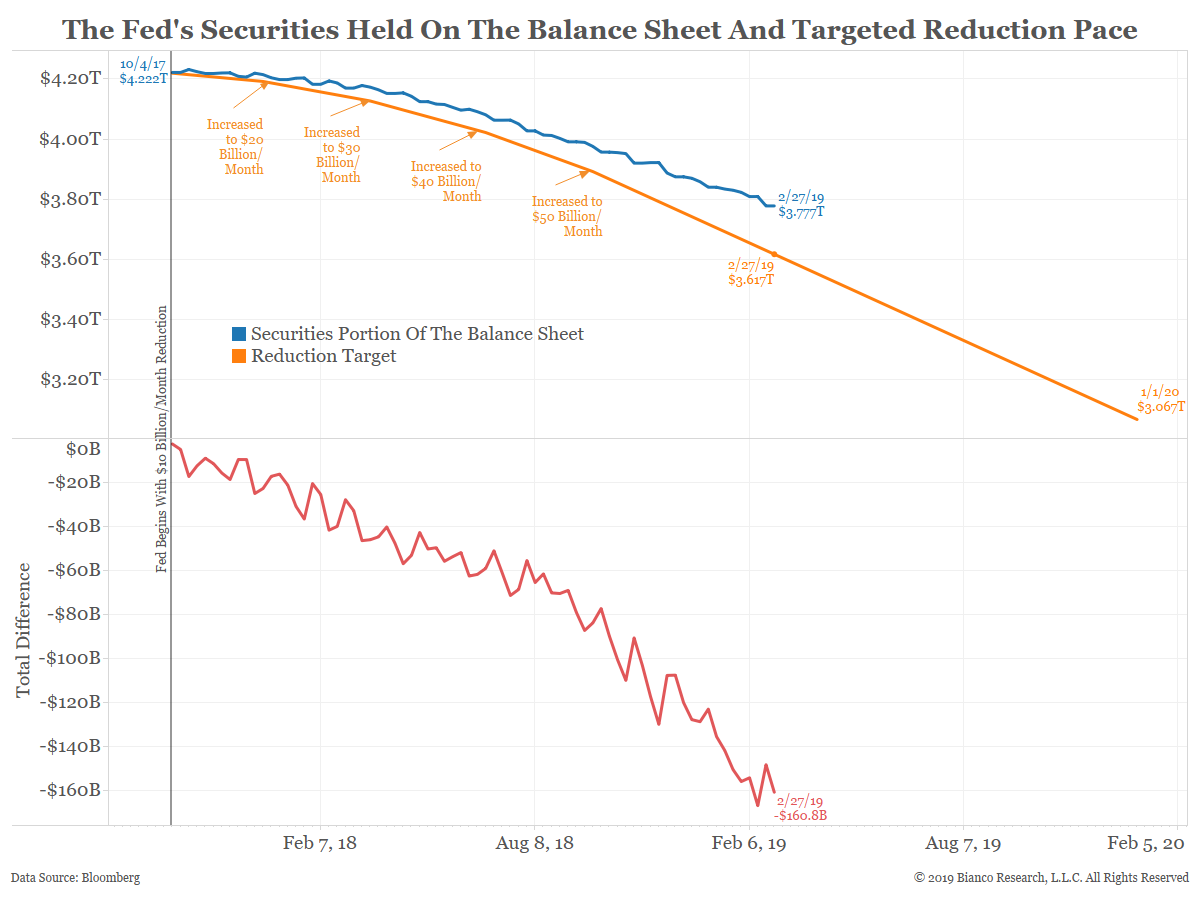

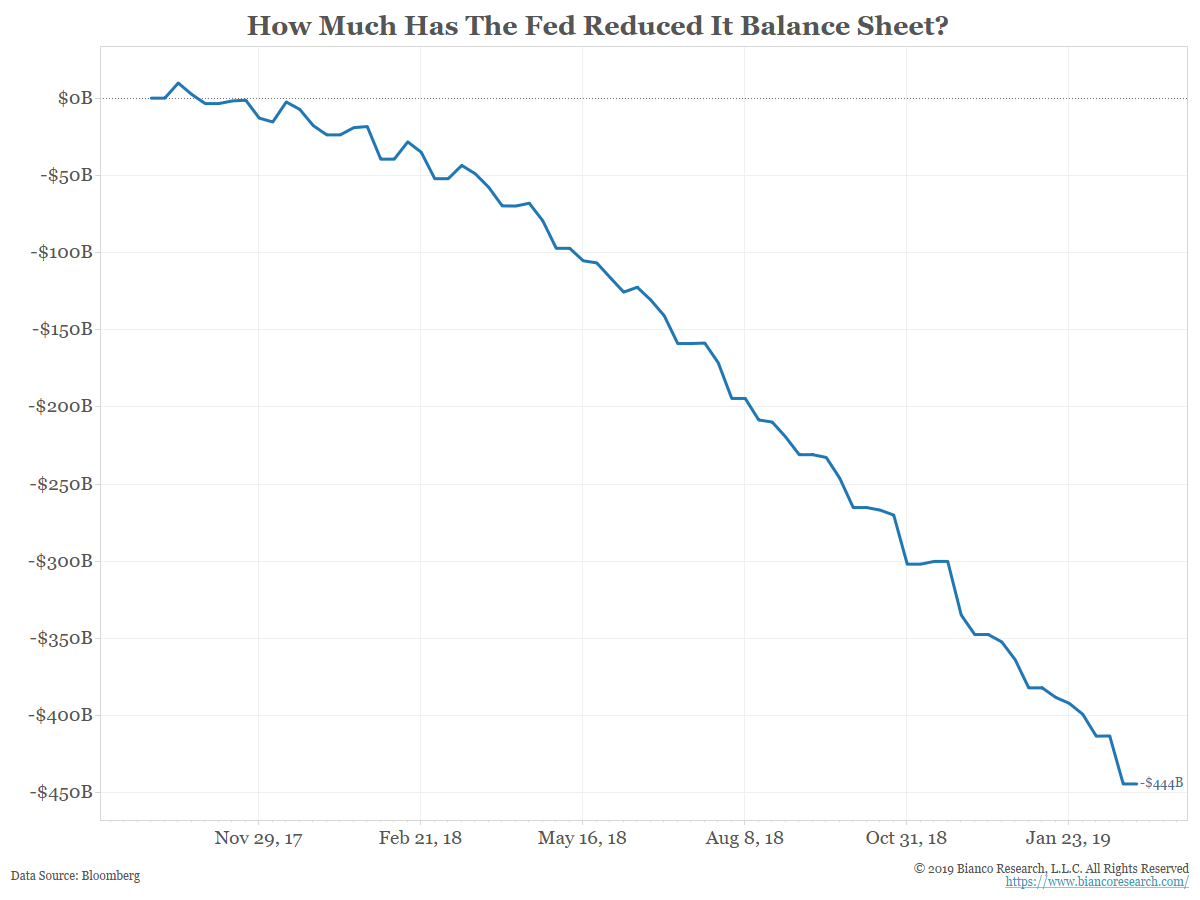

In 2017 the Kansas City Fed conducted a study on the effects of balance sheet normalization. In a nutshell, they stated a $675 billion reduction in the balance sheet was roughly equal to a 25 bps hike. So a $600 billion reduction in 2019 would be the equivalent of less than one hike. Further, as the chart below shows, the actual reduction to date has been around $450 billion, or about two-thirds of one hike, according to this measure.

Going forward, as the chart above suggests, the balance sheet should fall another $500 billion. In total, the Fed’s study suggests the total balance sheet reduction from October 2017 to the end of this year is the equivalent of 1.25 rate hikes.

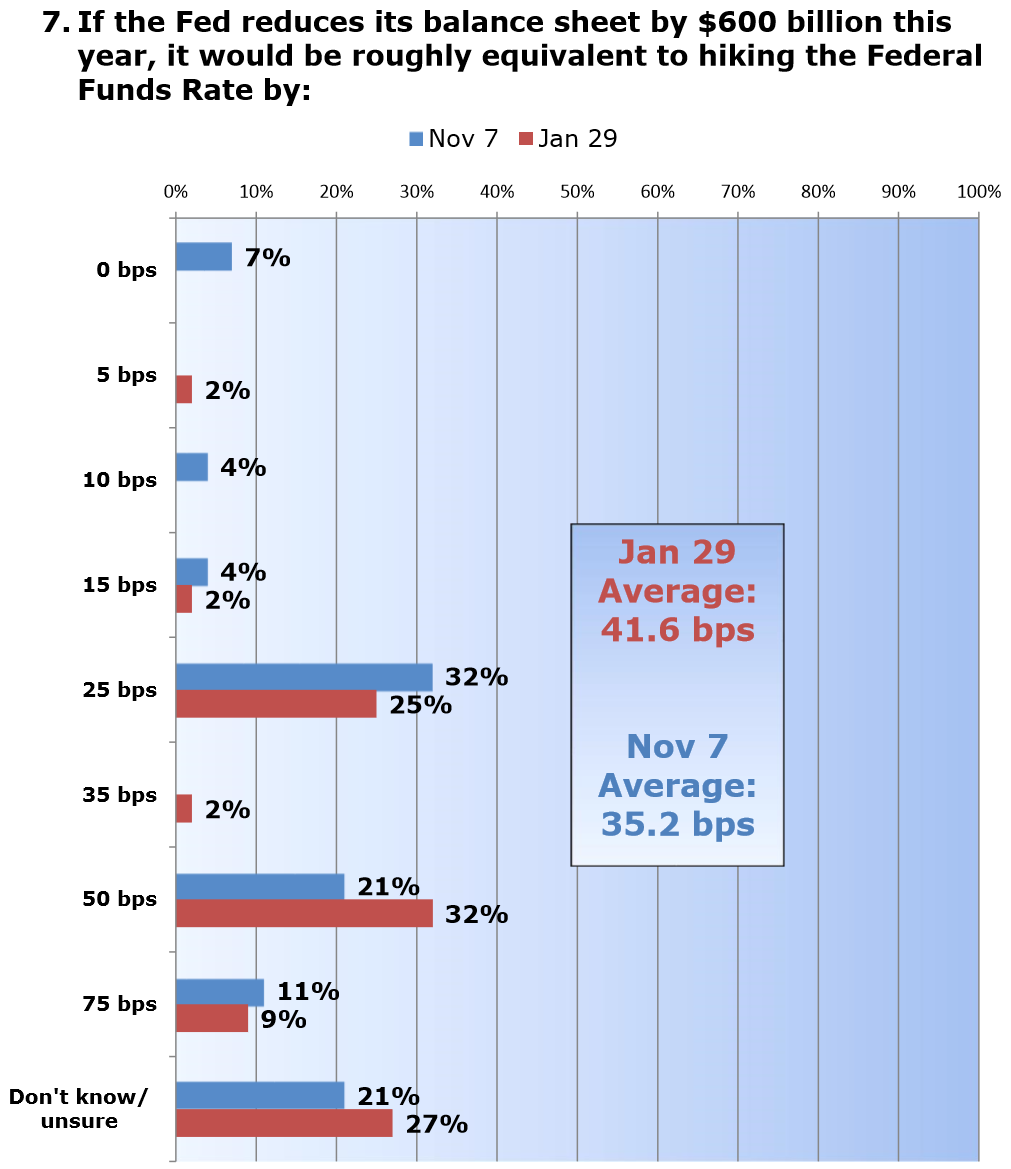

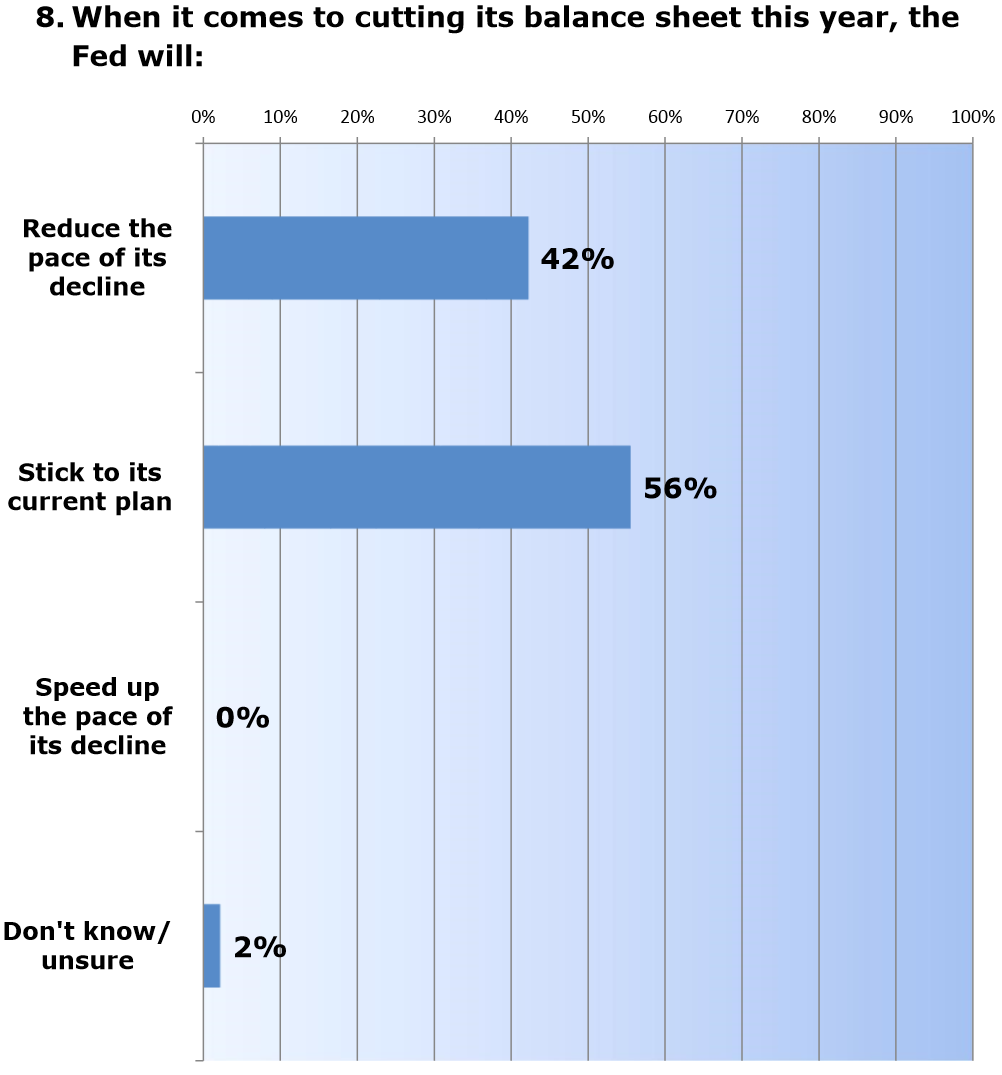

The participants in this survey think a $600 billion reduction is the equivalent of 41 basis points of tightening. 42% of respondents think the Fed should reduce the pace of the decline. This is a far more aggressive effect than the Fed believes it to be.

The market sees balance sheet reductions as a loss of liquidity, which is one of the main reasons for the difference in opinion. As the balance sheet dwindles, someone in the private sector has to replace the demand for those securities. While the Fed likely understands this, they may not be as acutely concerned about it as market participants.

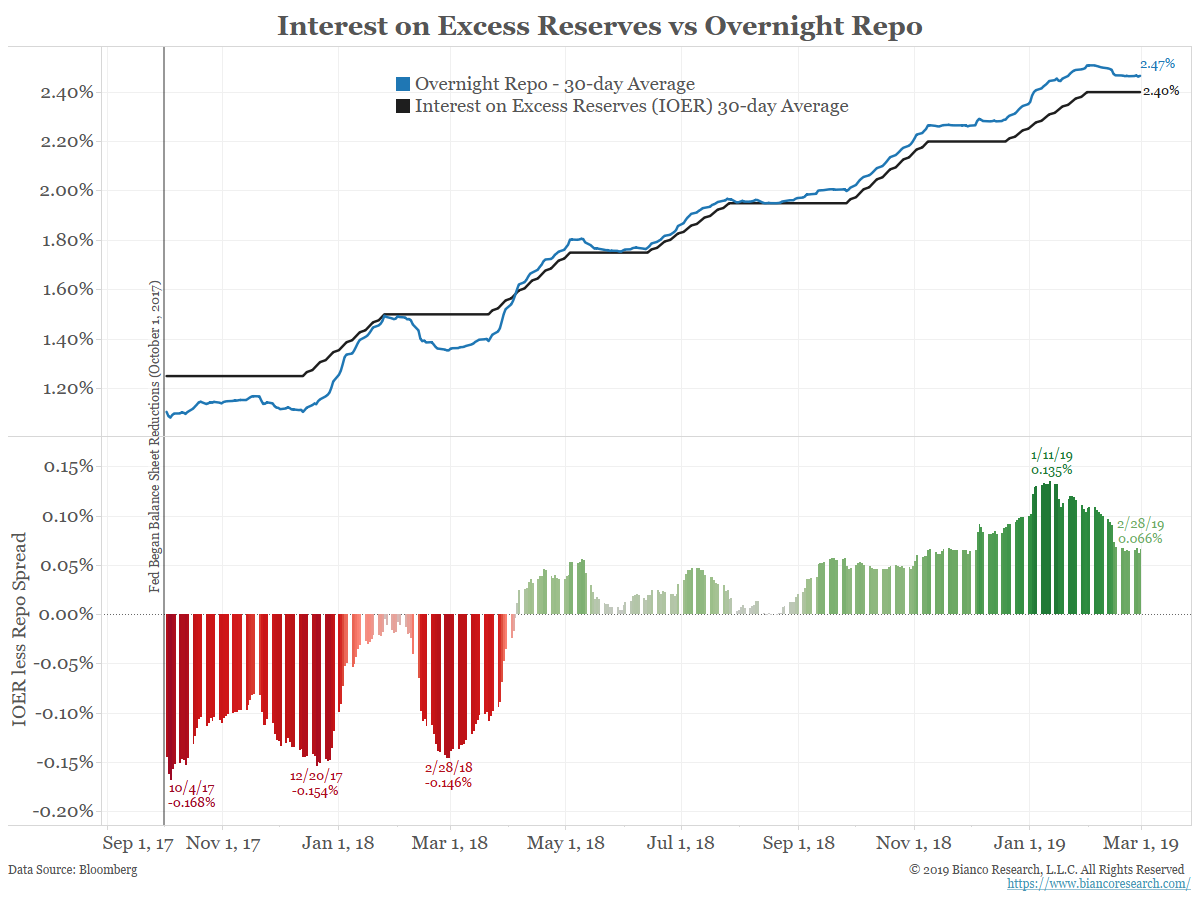

The next chart focuses on the overnight repo yields and IOER since balance sheet reductions began, using a 30-day average to remove the noise.

The bottom panel shows the difference between these two measures. The green bars signify repo yields are moving above IOER, evidence the funding markets have become tighter.

From the time the Fed started reducing its balance sheet until now, this spread has increased roughly 23 basis points, the equivalent of almost one rate hike.

Conclusion

The Fed is probably correct that the reduction in the balance sheet means little for reserves or bank lending and that its impact on jobs and GDP will be minimal. But, the market is also correct that the Fed is no longer buying securities, which means the private sector must step up to absorb that supply.

Neither side is incorrect in its view, but the difference in opinion was the source of much anxiety in the markets in December. As balance sheet reductions are expected to be coming to an end, the hope is that the Fed and the market’s views will be better aligned.