- Bloomberg.com – Powell Gets Sharp Warning From Senator Over Fed Inflation Target

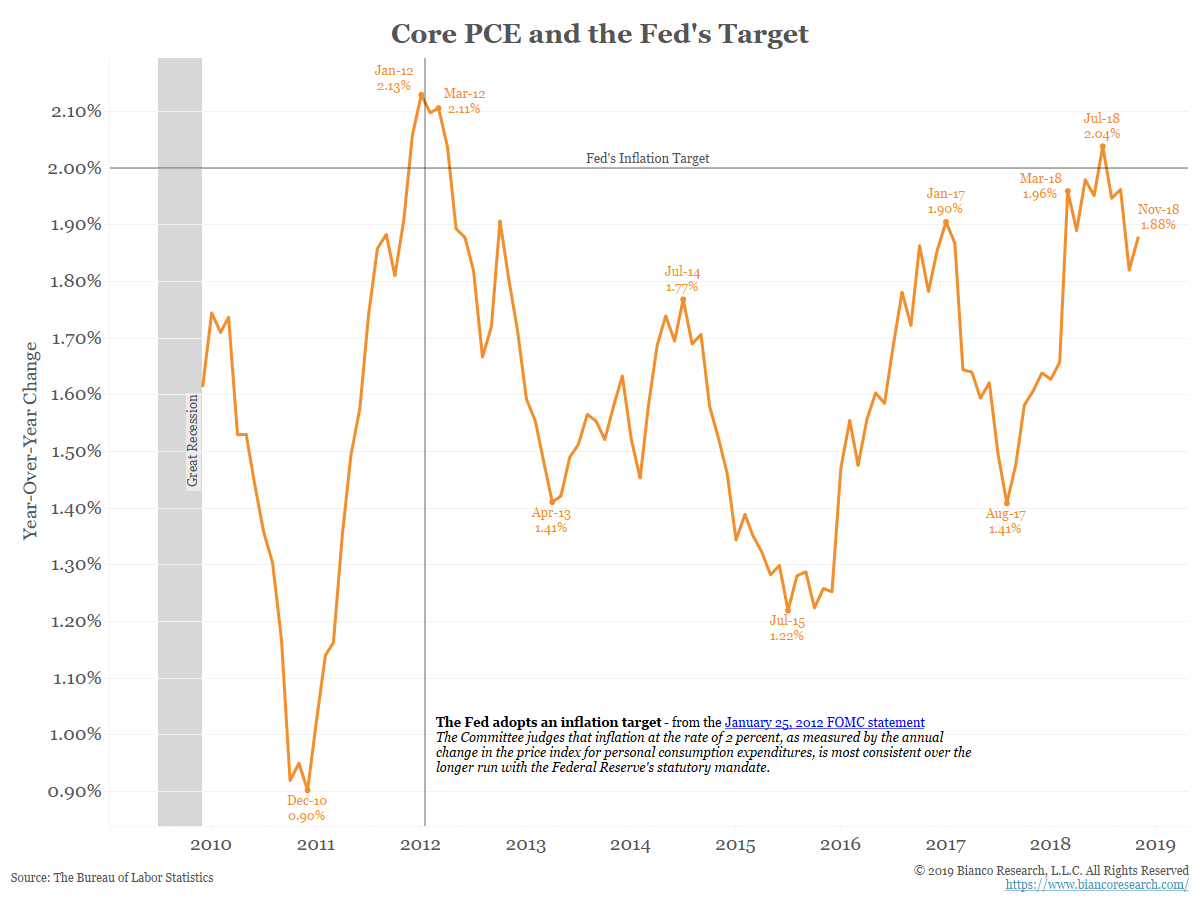

Low interest rates over the past four decades have made it more likely that the Fed’s policy rate will drop to zero again during future recessions, Powell said, making it more difficult for the central bank to stimulate economic growth. That, in turn, may help lower inflation expectations, a force Powell called “the most important driver of actual inflation.” “We’re trying to think of ways of making that inflation 2 percent target highly credible, so that inflation averages around 2 percent, rather than only averaging 2 percent in good times and then averaging way less than that in bad times,” Powell said during his testimony before the Senate Banking Committee.

Summary

Comment

In yesterday’s testimony Powell said the following regarding inflation expectations:

In our thinking, inflation expectations are the most important driver of actual inflation.

While most economists might see this as a statement of the obvious, we see a couple issues with it. For starters, true Inflation expectations are nearly impossible to measure. Even if they were easily measurable, we would question their ability to drive actual inflation.

Do Expectations Drive Inflation?

Micheal Shedlock (Mish) addressed this idea yesterday:

- Mish Talk (blog) – Stupidity Well Anchored: Absurdity of Inflation Expectations in Graphic Form

The idea behind inflation expectations is that if consumers think prices will go down, they will hold off purchases and the economy will collapse. The corollary is that is consumers think inflation will rise, they will rush out and buy things causing the economy to overheat.

Mish details how inflation expectations do not really drive purchase decisions and thus do not affect inflation. He also notes the irony that expectations can actually drive asset prices like homes and stocks. But, this is not the goal of the Fed.

He also notes that Lael Brainard sees issues with long-term inflation expectations:

“There is no single highly reliable measure” of longer-run inflation expectations, Fed Governor Lael Brainard told The Economic Club of New York on Sept. 5.

How To Measure

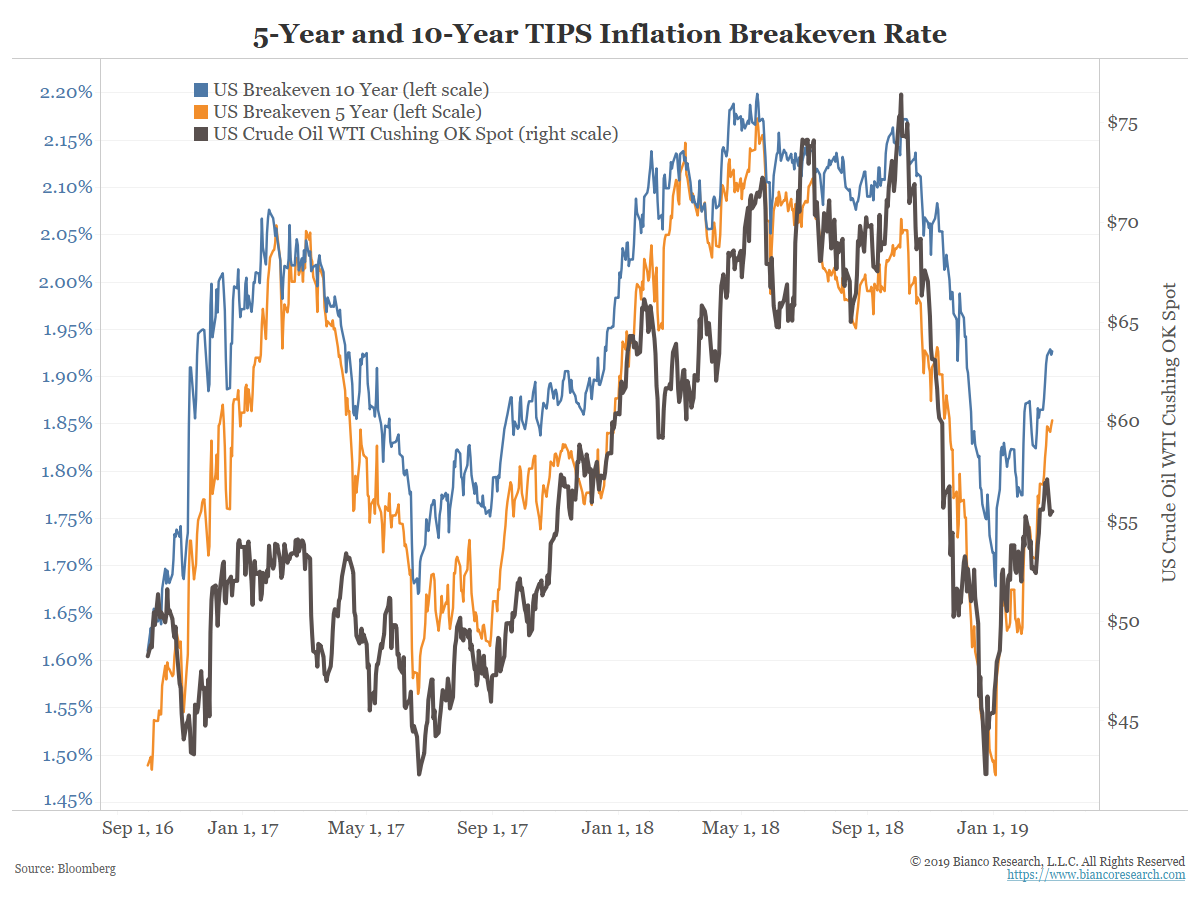

Inflation expectations come in two forms, market-based measures and surveys. Treasury Inflation Protected Securities (TIPS) breakeven rates are one of the more popular market-based measures of inflation expectations.

The black line in the chart below shows WTI crude oil prices. The orange shows the 5-year inflation breakeven and the blue line shows the 10-year inflation breakeven.

The energy sector, both commodities and services, only account for 7.1% of the overall CPI (December 2018). While this sounds small, the chart shows WTI prices move in tandem with inflation expectations.

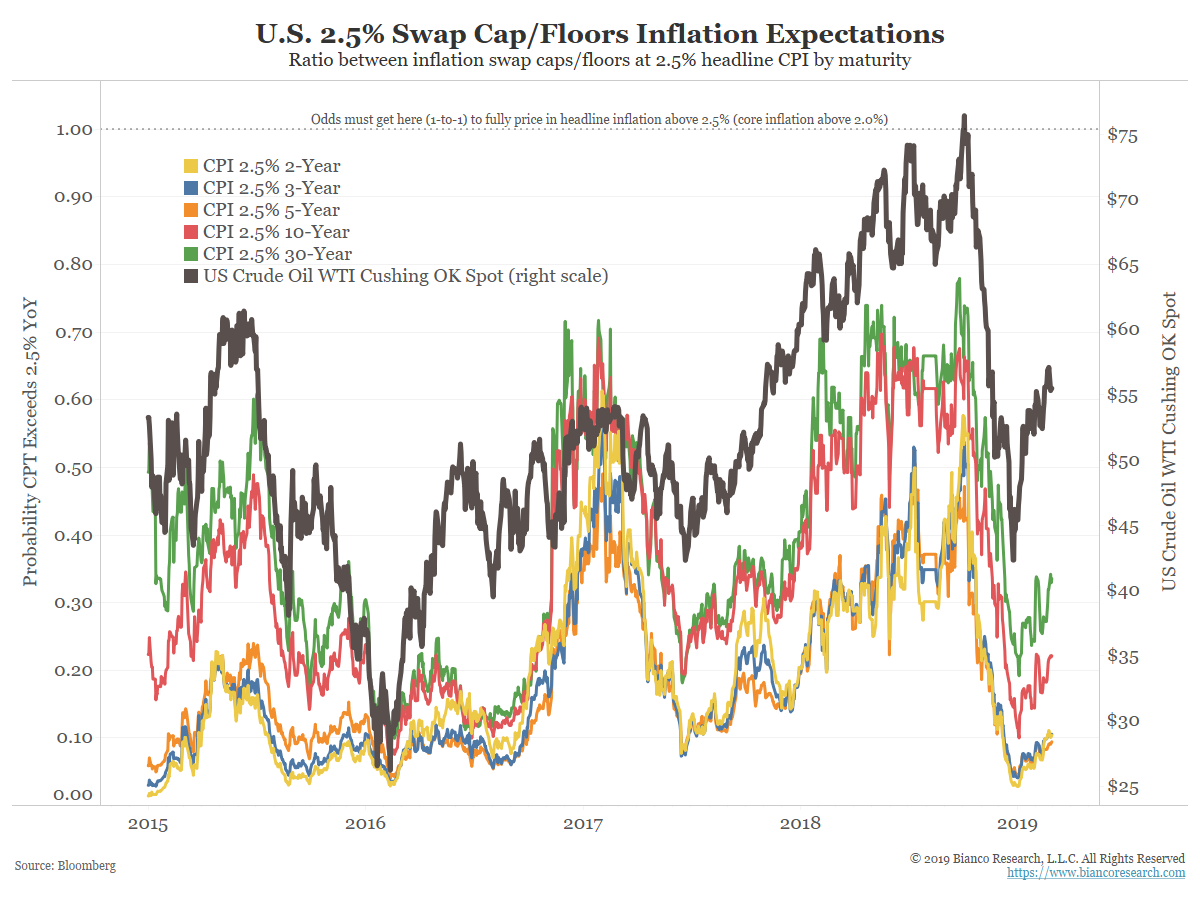

Inflation swaps/caps are another popular market-based measure of inflation expectations.

The thick gray line (right scale) below shows crude oil prices while the colored lines show the market’s opinion on inflation remaining above 2.5% over various time frames (left scale). The correlation is not as tight in this case, but when crude has sharp moves like it has the last few months, inflation expectations react. So even this measure, that is supposedly insulated from energy prices, seems to react when energy prices have a hard move.

Surveys

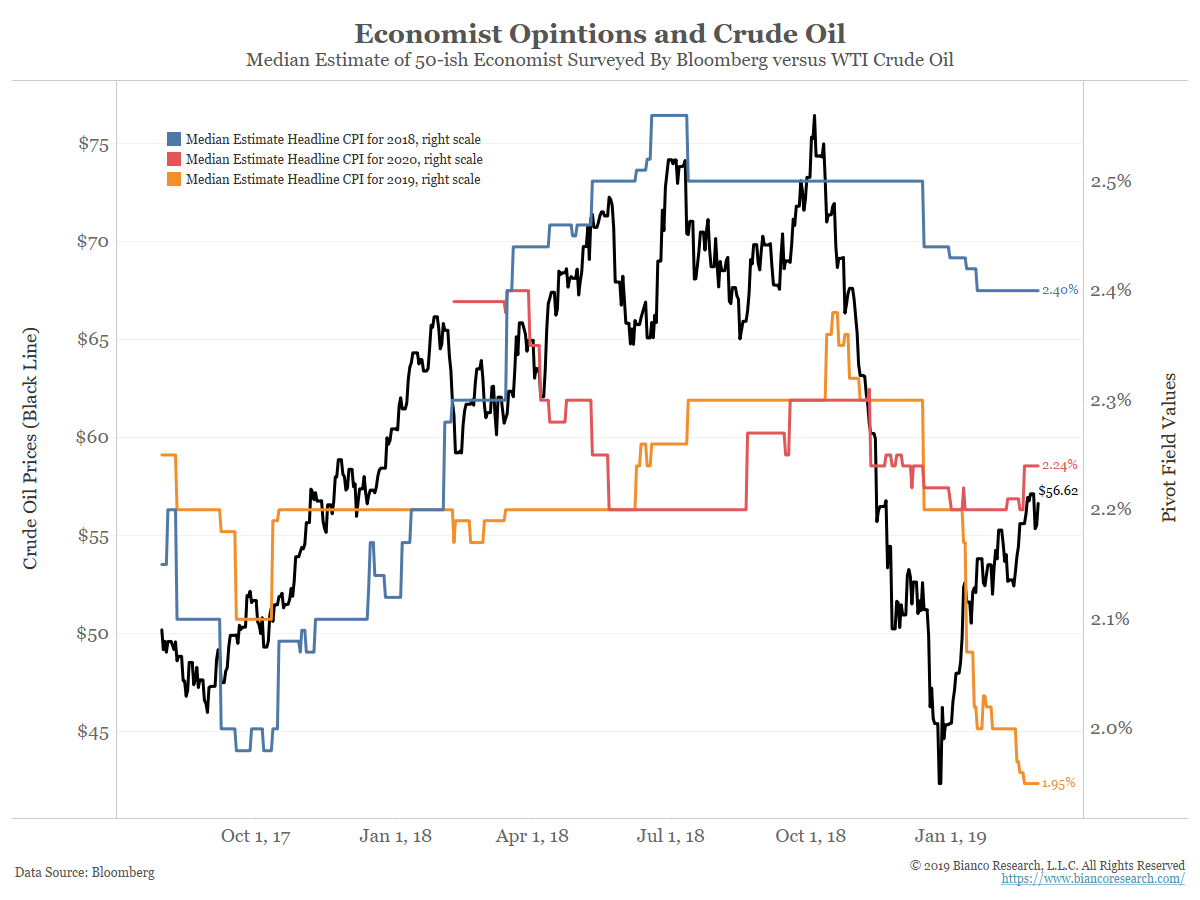

The next chart shows crude oil (black) overlaid on year-end inflation forecasts from a Bloomberg survey of over 50 economists.

When crude oil was rising in 2017 and early 2018, the 2018 forecasts for inflation (blue) were rising. When crude oil was collapsing in late 2018, the 2019 forecasts for inflation (orange) were falling. The relationship between crude and this measure of inflation expectations is apparent.

Conclusion

We believe it is dubious that inflation expectations are drivers of actual inflation as Jay Powell said. Even if so, it is next to impossible to find a reliable measure of expectations. Those that exist are heavily influenced by crude oil prices, a concept that would make the Fed uncomfortable. In the end, the Fed is setting policy on a debatable proposition that is impossible to measure.