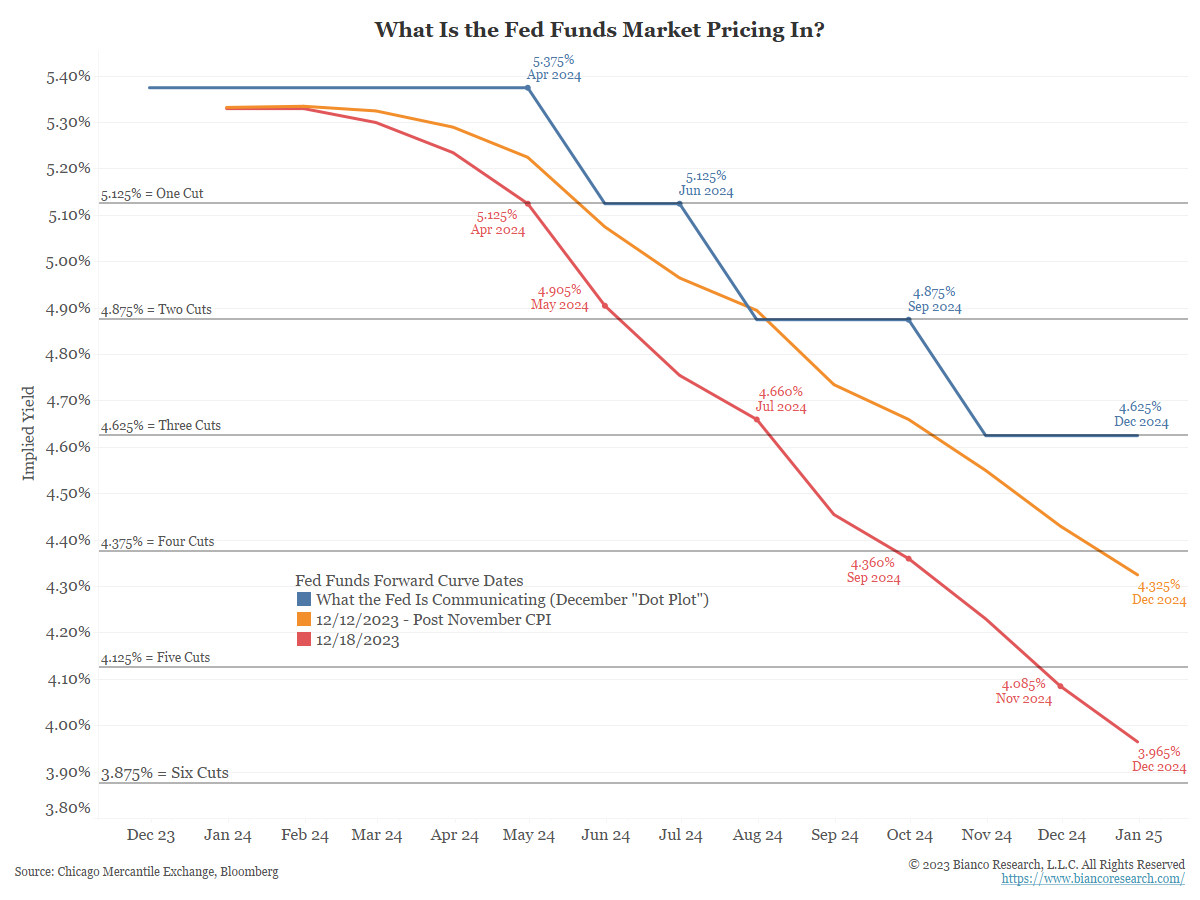

Introducing Our Index & Our 2024 Outlook

Join us Thursday, December 21, 2023 for our next conference call. ... Read More

Join us Thursday, December 21, 2023 for our next conference call. ... Read More

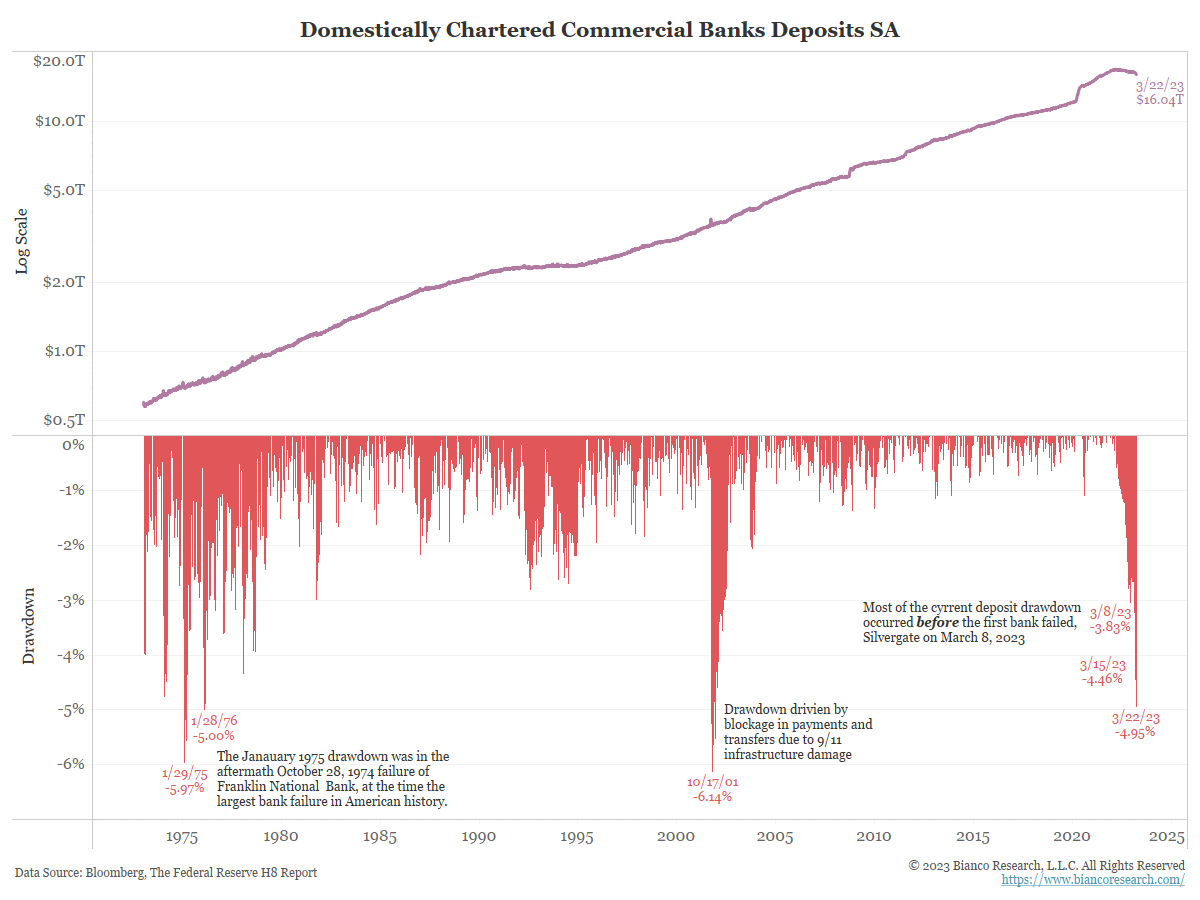

We keep returning to the issue of depositors withdrawing funds from banks for higher-yielding alternatives. This is a liquidity crisis impacting the liability of side of the banks' balance sheets. Banking data released late last week show the problems are not yet over.... Read More

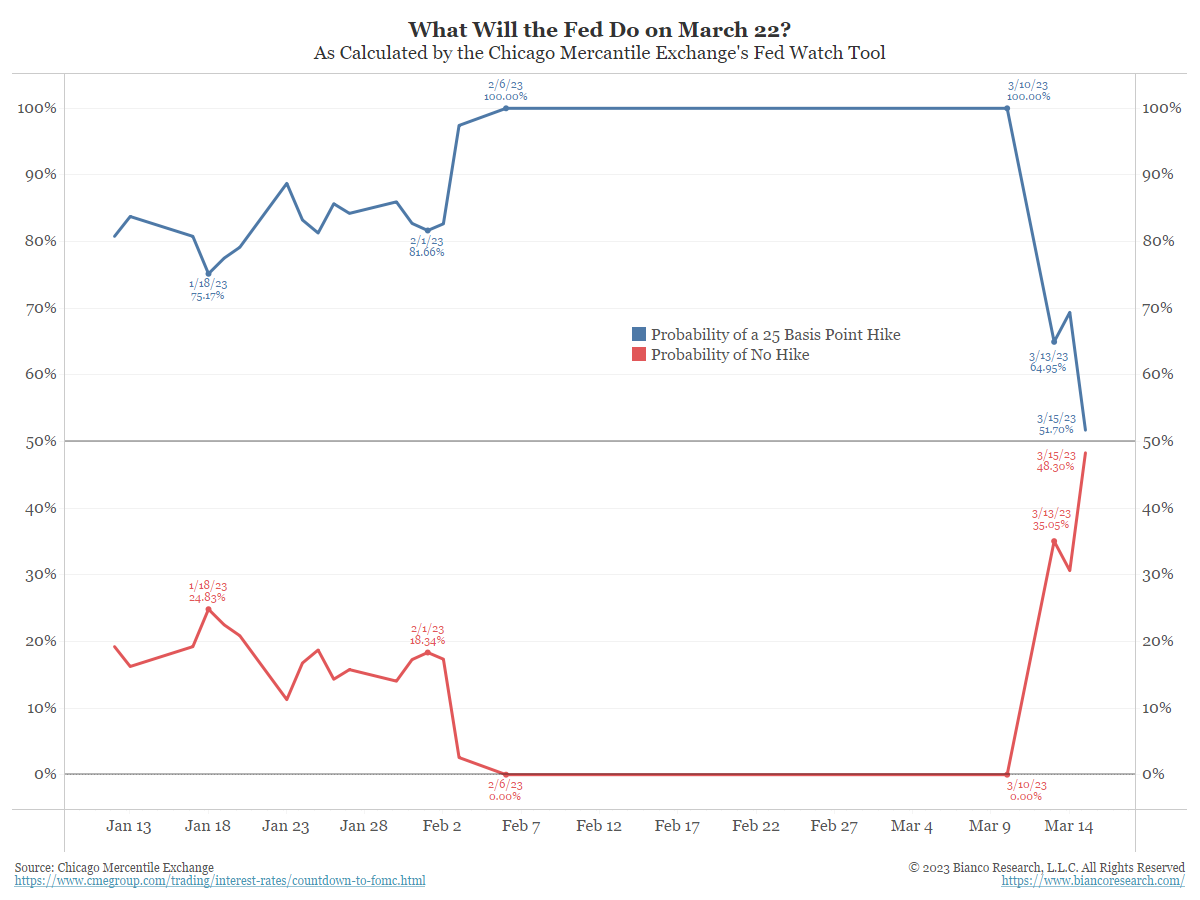

In this confusing environment, we believe the Fed will take its cue from the stock market in deciding what to do next week.... Read More

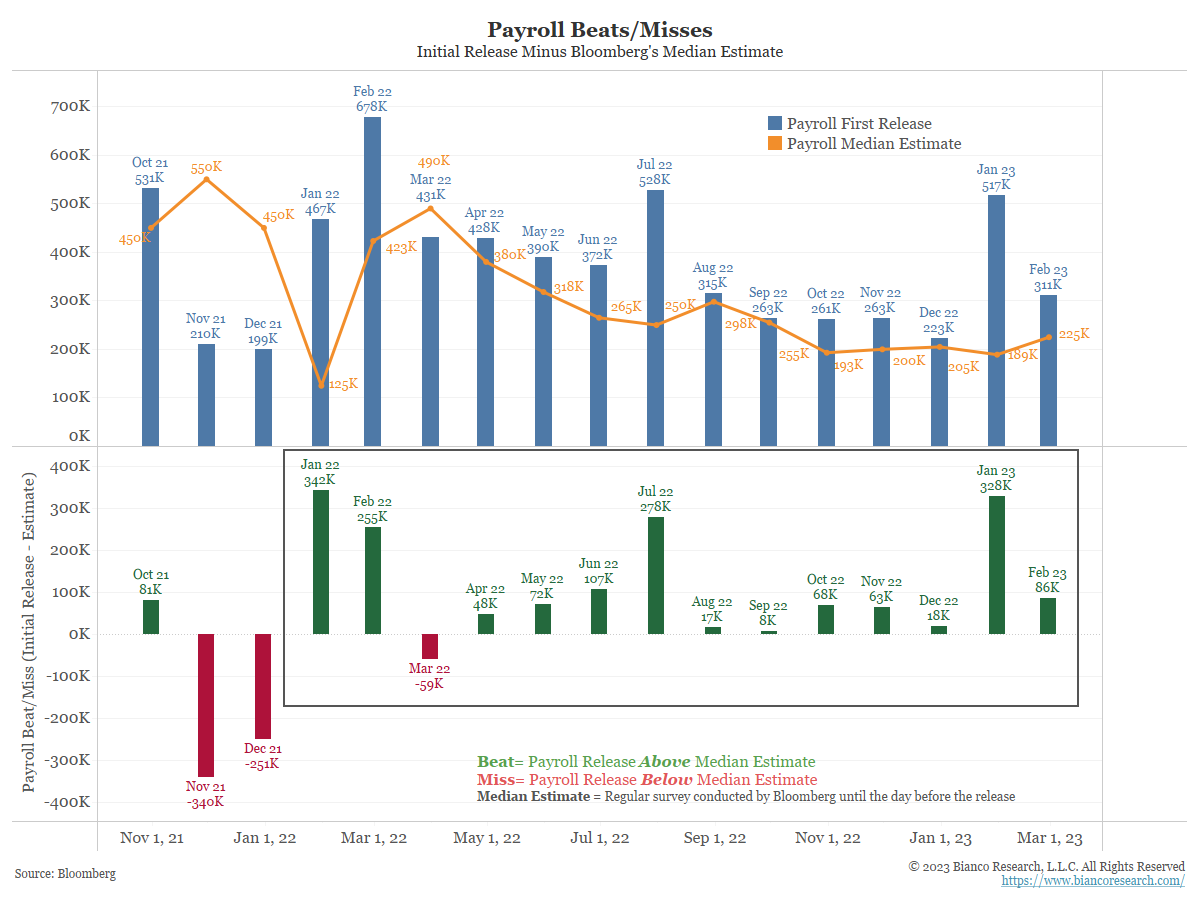

Payrolls beat expectations for a record 11th straight month. Despite another beat, the fed funds market remains split on whether the Fed will hike 25 basis points or 50 basis points on March 22.... Read More

In the latest installment of Talking Data, Jim discusses the payrolls survey and survey response rates. ... Read More

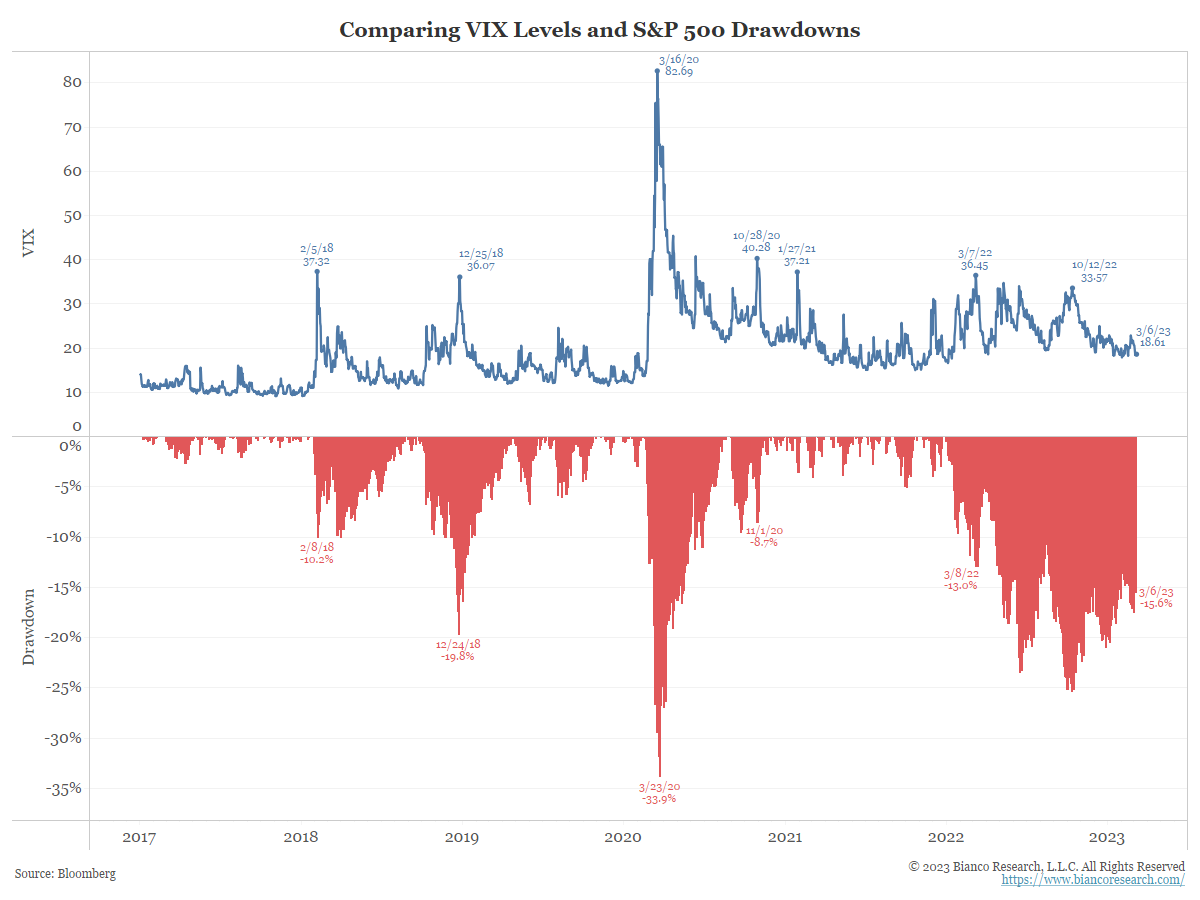

While intraday volatility rises, longer-term volatility remains subdued. Traditional measures of volatility are being questioned. Understanding how this happened might give a clue as to where the risk lies.... Read More

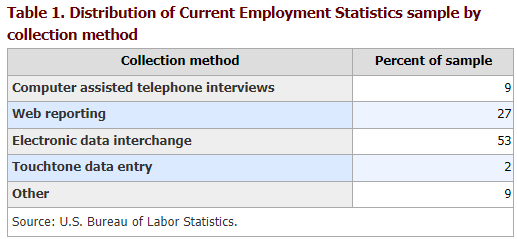

Many government statistics are collected via surveys. As with political polls, the public is souring on answering them. The result is lower response rates and larger error rates.... Read More

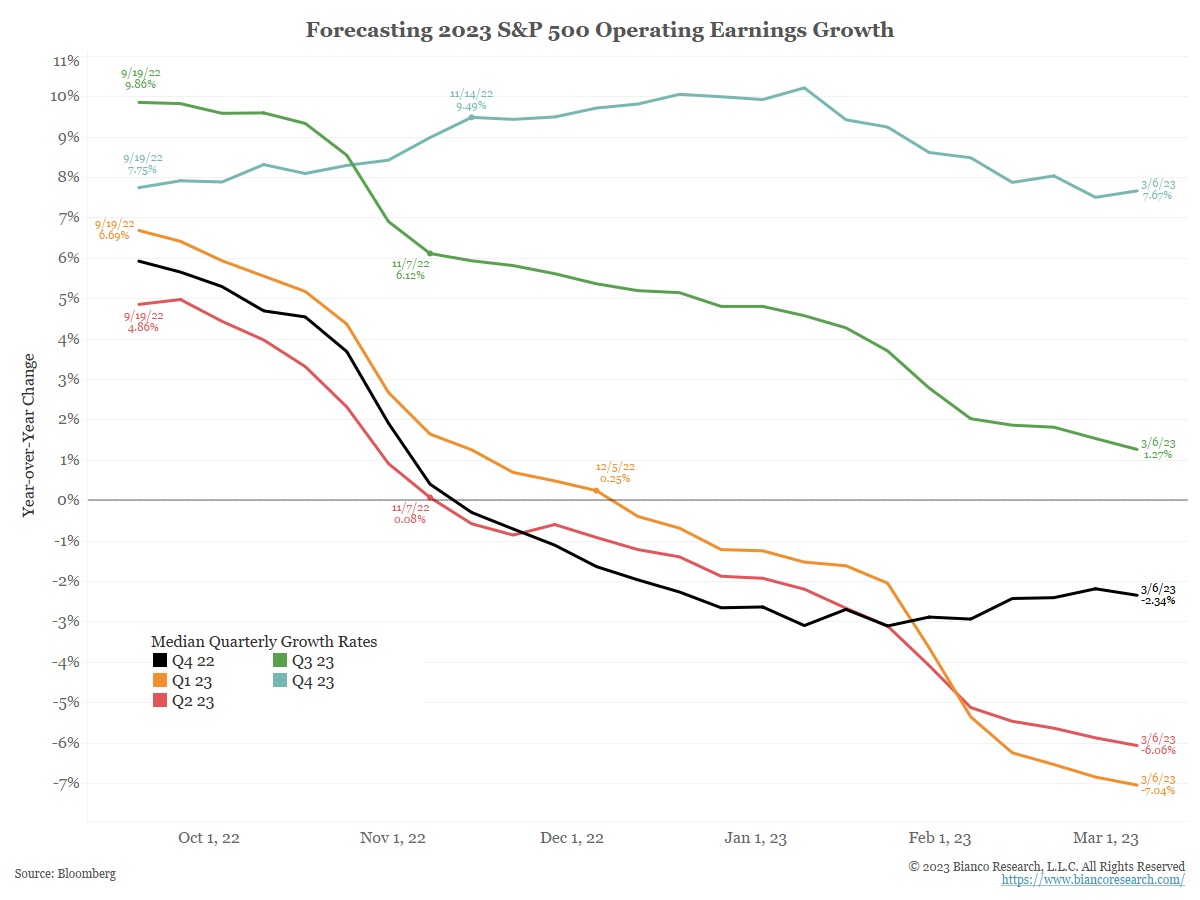

As the Q4 2022 reporting season winds down, earnings have been a disappointment. The beat rate is less than expected and the reporting "bounce" is among the smallest ever seen.... Read More

In the latest installment of Talking Data, Jim discusses expectations for a recession and the role of rates. ... Read More

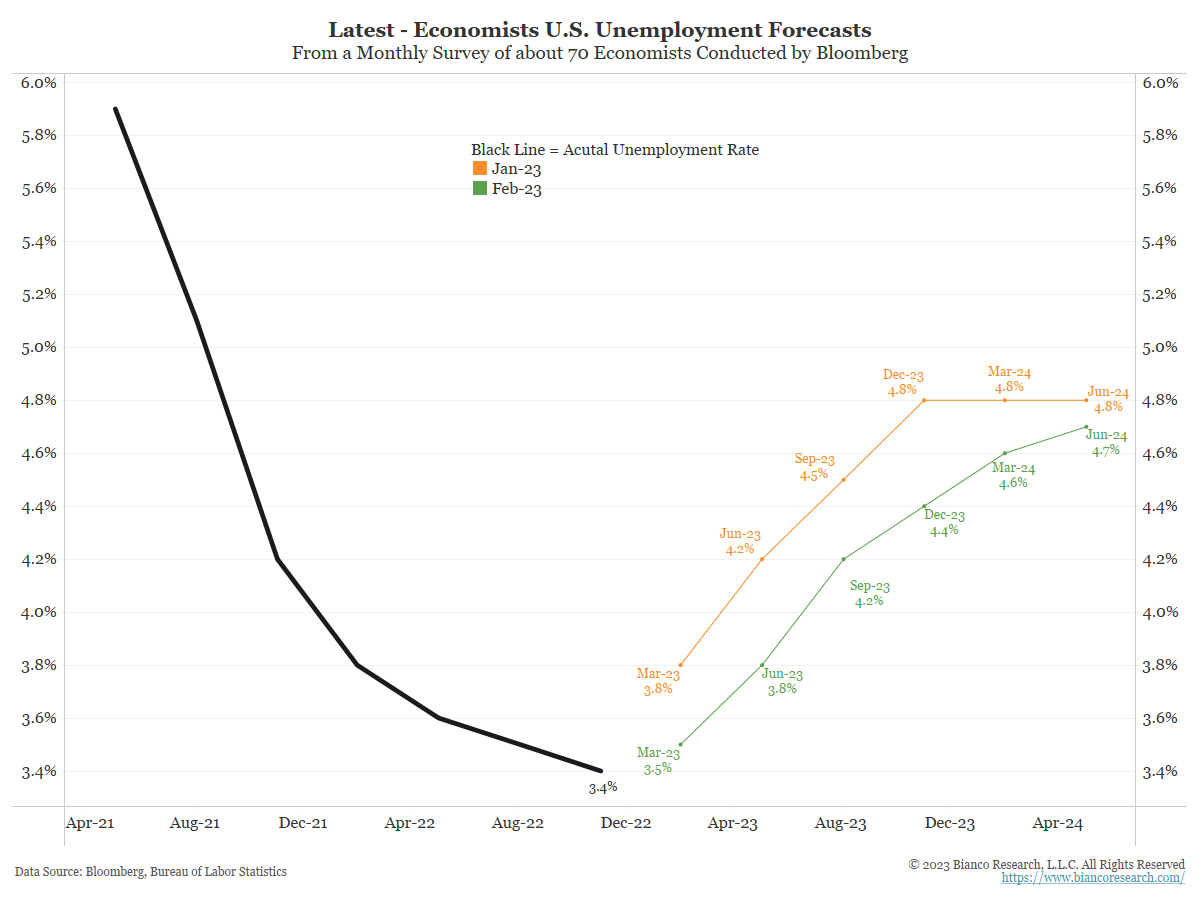

The latest updates to the consensus economic view are more of the same. A recession is coming, unemployment will soar, and inflation will return to 2%. This outlook has been wrong for over a year. With all the forecasting errors in the same direction, what are economists missing?... Read More